Structured Investment Strategies

A Comprehensive Investment Framework

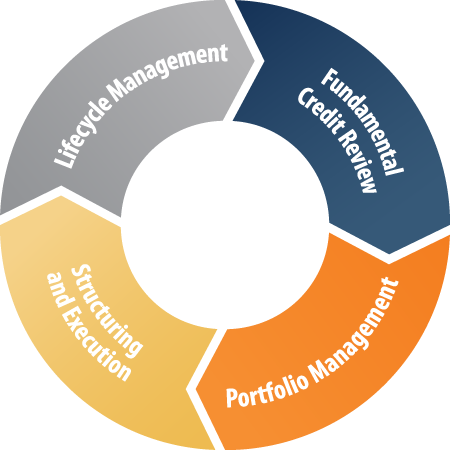

Our investment approach seeks to maximize the potential benefits of structured notes while carefully managing the associated risks. We combine disciplined credit analysis, active portfolio management, and thoughtful structuring which enables us to remain agile and responsive throughout the lifecycle of the notes, with a clear focus on optimizing returns and protecting investor capital.

Continuous Portfolio Oversight

Credit Review: Safeguarding Credit Quality

The fixed income sub-committee of First Trust’s Investment Committee conducts a fundamental credit review each month, evaluating the creditworthiness of the issuers. This ensures high credit quality and allows us to swiftly adapt to any changes in market or issuer conditions. Structured investment issuers are continuously monitored for their credit health.

Portfolio Management

Our investment team is responsible for portfolio construction and monitoring, carefully selecting and managing the notes to balance optimal portfolio positioning with risk diversification. They continuously assess performance and risk factors, including protection levels and investment limits, to ensure that the portfolio remains aligned with the strategic objectives. Key elements of this process include:

- arrow_right Portfolio positioning and diversification aligned with strategy objectives and constraints.

- arrow_right Setting return targets and strategy exposures with attention to valuations and risk factors impacting each structured note.

- arrow_right Daily oversight of performance and risk factors, relative to structure protection levels, investment limits, and alignment with strategic objectives.

Structuring and Execution

Our structuring desk works seamlessly within the investment process, structuring notes through competitive auctions and leveraging ongoing market insights to secure favorable terms. This enables us to customize notes by issuer, maturity, and underlying equity exposure, aligning them with our strategy and risk tolerance.

Lifecycle Management: Active Monitoring Throughout

We remain engaged across the entire lifecycle of each investment:

- arrow_right Continuous monitoring of life cycle events such as calls, maturities, and coupon payments.

- arrow_right Agile response to market shifts and issuer developments.

- arrow_right Ongoing assessment to maintain portfolio resilience and identify opportunities.

Risk Considerations

This is not an offer to buy or sell any security and does not include a complete list of all securities purchased or sold in the period or for all clients. Actual holdings will vary and there is no guarantee that any client will hold any mentioned positions. No security or discipline is profitable all of the time and there is always the possibility of loss.

There is no assurance that a separately managed account (“SMA”) will achieve its investment objective. Accordingly, you can lose money investing in an SMA. SMAs are subject to market risk, which is the possibility that the market values of the securities in an account will decline and that the value of the securities may therefore be less than what you paid for them. The value of investments held by the strategy may increase or decrease in response to economic, financial, and political events (whether real, expected, or perceived) in the U.S. and global markets. It is difficult to predict the timing, duration, and potential adverse effects (e.g., portfolio liquidity) of events.

High portfolio turnover may result in higher levels of transaction costs and may generate greater tax liabilities for shareholders.

While SMAs can be customized, accounts with smaller balances may struggle to achieve optimal diversification across multiple asset classes due to the higher cost of individual securities.

Fees associated with SMAs can be higher than mutual funds and ETFs that include manager, service, and advisory fees. Being able to withdraw cash from an SMA may be delayed due to the amount and type of positions to be sold. Withdraws may negatively impact the SMA’s performance.

Structured investment strategies are considered complex, risky and are not appropriate for all investors.

Structured notes offer a wide variety of features, with attributes which affect their risks and potential rewards. Before making any investment decision, an investor should refer to a structured note’s offering documents for additional information and obtain advice from their financial, legal and tax professionals for information about and analysis of the investment, its risks and its appropriateness in their particular circumstances.

Structured notes lack liquidity. Structured notes are not listed on any securities exchange and an investor may not be able to sell a structured note prior to maturity. An issuer may offer to purchase a structured note in the secondary market, but it is not required to do so. The price, if any, at which an issuer may be willing to purchase a structured note in the secondary market, if at all, may result in significant loss of principal. An investor should be able and willing to hold a structured note to maturity.

Structured notes are classified as senior unsecured debt. Payment on a structured note is subject to the credit risk of the issuer. Credit risk means that if the issuer were to default on its payment obligations, the structured note investor may not receive any amount owed under the structured note and could lose their entire principal investment.

The potential return on a structured note is subject to market volatility and the risks associated with the reference asset. The return of a structured note may be zero or less than what could have been earned on a traditional fixed income security.

Structured notes are not deposit liabilities or other obligations of a bank and are not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other governmental agency or program of the United States or any other jurisdiction.

This summary is not intended to be tax or legal advice. This summary cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on the taxpayer. This summary is being used to support the promotion or marketing of the transactions herein. The taxpayer should consult an independent tax advisor regarding the U.S. federal income tax consequences of an investment in the notes in the Strategy.

The information presented is not intended to constitute an investment recommendation for, or advice to, any specific person. By providing this information, First Trust is not undertaking to give advice in any fiduciary capacity within the meaning of ERISA, the Internal Revenue Code or any other regulatory framework. Financial professionals are responsible for evaluating investment risks independently and for exercising independent judgment in determining whether investments are appropriate for their clients.